Negative EV, Profitable, Share Buybacks, Hidden Software Business

Over the past year, I’ve followed an investing rule that has served me well:

Whenever a consistently profitable company trades below net cash in an English-speaking country, stop everything and take a closer look.

In my experience, these situations rarely last. They are usually temporary, caused by excessive pessimism or fear about the company. Sentiment that often shifts as soon as the next quarterly results are released.

Today’s stock fits this criteria. It has grown rapidly over the past decade, remains profitable, and is currently trading at a negative enterprise value due to what I believe is a temporary setback.

While risks exist, setups like this often offer patient investors compelling asymmetric opportunities.

Let’s get started.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. Investing involves risk, including the potential loss of principal. The author may own, or plan to purchase, shares in the security discussed. The author is not a registered investment advisor and does not provide personalized investment advice. Always conduct your own research and consider your investment objectives and risk tolerance before making any investment decisions. The author and publisher shall not be liable for any actions taken based on the information provided in this article.

Note: all values in NZ$

Summary:

Solution Dynamics Ltd (SDL.NZ) is a New Zealand based company operating in the global customer communications market.

The company operates two business segments:

Services (42% of revenue): SDL’s legacy print and mailhouse operations, based in New Zealand. The business handles high-volume digital printing and document distribution (such as bank statements, invoices, and promotional mail) while outsourcing postage, logistics, and third-party printing.

Software (58% of revenue): SDL’s SaaS and managed services platform. It enables enterprises to manage personalized, compliant, multichannel customer communications at scale. This segment has experienced strong growth as corporations have shifted to digital communications over physical mail.

Despite its small size, SDL has maintained a strong presence in New Zealand for decades. The company was founded in 1996, initially operating as a traditional mailhouse. SDL listed on the New Zealand Exchange in 2004 and gradually developed proprietary software to broaden its service offerings. A significant milestone occurred in 2018 with the acquisition of DigitalToPrint in the United States, which expanded SDL’s international software business and provided the infrastructure to expand internationally.

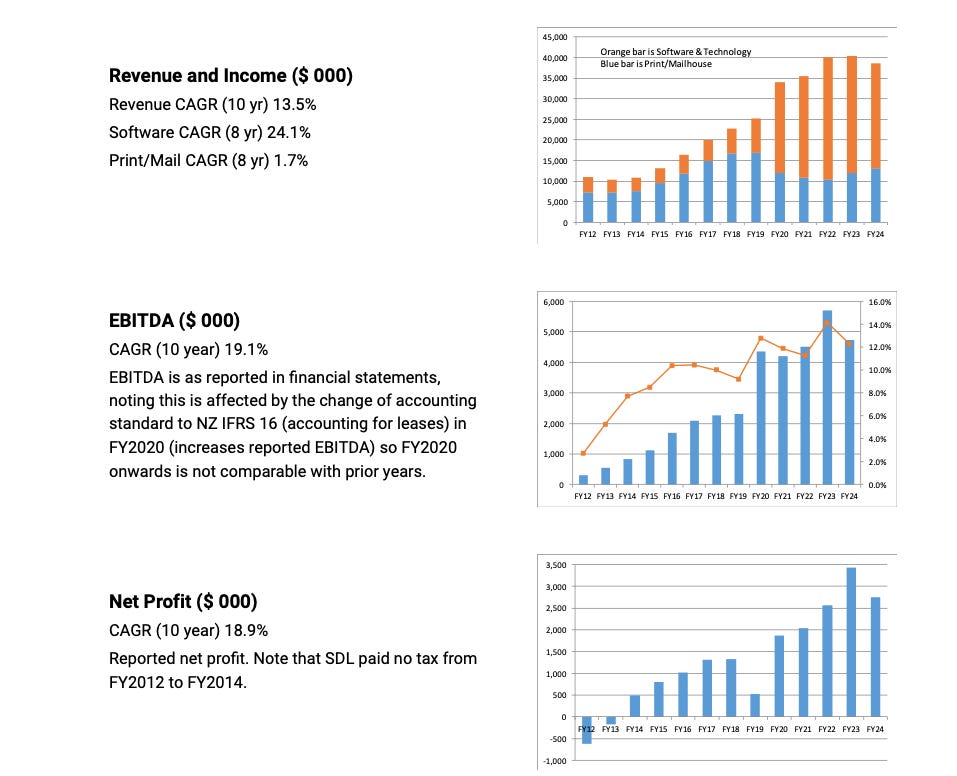

SDL has succeeded in capturing market share from larger players and expanding both their services and software business, resulting in compounding revenue and net income at a 19% CAGR over the past decade:

Something that stood out to me as I began to research this company was the disconnect between perception and the actual underlying business fundamentals. While it is categorized as an old-fashioned print company, SDL operates in a way that makes it a fantastic business.

In the Services segment, SDL leases print/mail equipment and outsources postage and logistics. These pass-through costs are handled at low margins but without the heavy capital requirements of traditional printers.

The software segment requires no physical assets, and revenue scales with little incremental investment.

The result is a business with almost no PPE on the balance sheet, minimal working capital needs, and Capex consistently below 2% of operating cash flow. Nearly all EBITDA converts to free cash flow, which can be returned to shareholders through dividends or buybacks. With growth being self-funded, ROIC is exceptionally high after netting out excess cash.

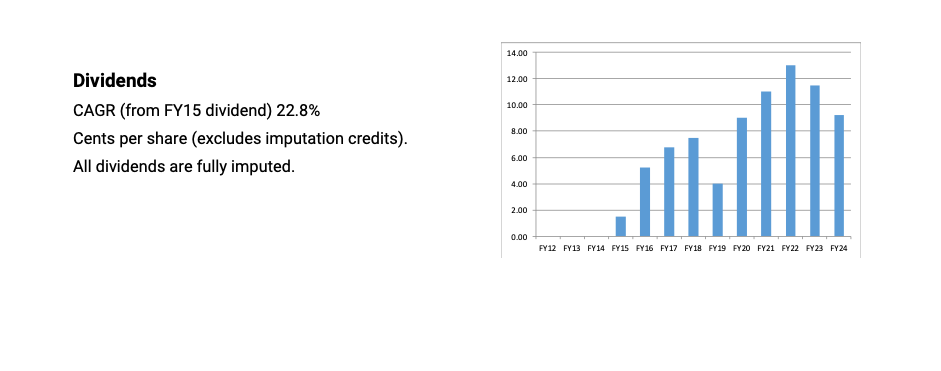

This allows SDL to scale without reinvestment, which explains how they have grown so quickly while historically paying out over 70% of net income as dividends:

Importantly, the software business is sticky. Once onboarded, clients rely on SDL’s platform for compliance and customer communications across multiple channels, making switching both costly and risky, especially for regulated industries such as banks and utilities.

SDL has used partnerships to scale efficiently. In 2020, the company struck a deal with U.S. based Pitney Bowes, under which SDL provides the software infrastructure for Pitney Bowes’ customer communication services across several major markets.

This arrangement is mutually beneficial: Pitney Bowes can offer SDL’s platform without investing in developing its own, while SDL gains access to Piney Bowes’ global customer base at effectively zero cost. This partnership resulted in a 40% revenue increase in 2020 and continues to support SDL’s international growth.

Setback Creates Opportunity:

In November 2024, SDL’s largest customer announced it would transition from a single supplier model to a multi-vendor model for the services SDL provided.

While SDL still serves this client on a project basis, this created an immediate impact on profitability and forced a restructuring of the company.

Shares crashed more than 40% on the news.

Management has not disclosed exact figures, but I estimate this customer represented 20-25% of total revenue.

While clearly a blow, I believe it creates an attractive setup after the share price collapse.

While the bearish argument would be that this is the first of many customer losses for a business in secular decline, there are a number of reasons I believe this is more likely to be a temporary setback:

The customer loss was purely due to commercial factors, not poor performance.

SDL is still servicing this customer on a project basis, with only one other vendor competing with them. Management has conservatively assumed zero revenue from this customer, although there is clearly the opportunity for significant revenue recovery.

The rest of the business is continuing to grow. SDL continues to gain market share in New Zealand, and international software revenue remains strong. In FY25, U.S. sales grew 27% and U.K. sales grew 33%. The remaining nine of the ten largest customers grew revenue by 21%.

Part of this growth reflects a deliberate shift in SDL’s sales strategy over the past few years, prioritizing the SaaS product over print mail services. This adjustment is expected to increase the share of revenue coming from the higher-margin software business, supporting both top-line growth and improved profitability.

Management guides FY26 net income of NZ$0.1-0.6M, down substantially from NZ$2.6M in FY25. However, I expect profitability to recover strongly over the next few years as the business continues to grow.

Management has also been very conservative with their guidance in the past, resulting in meeting or exceeding the top range in the past few years. I believe there is a strong likelihood that FY26 net income will exceed current forecasts.

The fact that SDL remained profitable even after losing a quarter of its revenue underscores the strength of its asset-light model, where costs were quickly reduced in proportion to the revenue loss.

Growth Drivers:

Aside from the large customer loss, there is currently a favorable environment for SDL to generate strong growth over the next 2-3 years:

Market share gains in New Zealand: With a large competitor exiting the country, SDL is poised to take additional market share in its home market. Even in a structurally declining industry, SDL has been able to grow its services revenues by gaining market share.

Three Waters reform: A government driven restructuring of New Zealand’s water utilities will create new entities that need to set up billing and communications systems from scratch, which is SDL’s core business. Management views this as a multi-year growth driver.

Mortgage refinancing tailwind: SDL has historically generated significant revenue from promotional mail campaigns tied to mortgage refinancing. Higher interest rates have dried up this revenue source and have been a large factor in revenues stagnating over the past few years. If interest rates fall, a new wave of refinancing would spur a recovery in this high-margin revenue source.

Valuation:

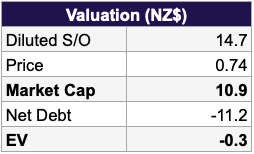

For most of the past decade SDL has traded at over 15x earnings. With the loss of their largest customer sentiment has completely shifted, and the market is now saying the company is worth more dead than alive. The current stock price is NZ$0.74, with NZ$0.76 of net cash per share.

At today’s price, investors are effectively getting a capital-light, high ROIC business for free.

I don’t think much has to go right to make money here. If the company can remain profitable and continue to grow even at a slower rate, the stock will eventually re-rate in line with its earnings power.

Even being conservative and assuming the company only recovers to $1M per year of net income (a third of last year’s earnings), a 10x earnings multiple plus net cash would value the company at ~NZ$21M, double the current price.

There is potential for additional upside should the market begin to value this as a software business and assign a multiple based on sales rather than net income.

Estimating upside in this situation is difficult, as it ultimately depends on how quickly SDL can recover lost revenue and profitability. However, I am attracted to this setup because the downside appears well protected at today’s valuation. Even in a bearish scenario, I believe the stock would not trade meaningfully lower than current levels, while any recovery could unlock substantial upside.

Management/Capital Allocation:

I believe the current leadership team is capable of returning the company to growth. CEO Patrick Brand was appointed in 2021 after running SDL’s international operations, where he was credited with record growth. He previously held senior roles at Pitney Bowes, giving him deep industry expertise at a multi-billion dollar company.

Management has been shareholder friendly throughout the restructuring. Board fees have been cut and the chairman’s fees were eliminated entirely.

They have also demonstrated a clear commitment to returning capital to shareholders. In 2025, management declared a 3 cent dividend, equal to 4% of the current market cap, as well as authorized a share buyback of up to 5% of outstanding shares. The board made their view explicit in the annual report:

“The directors are conscious of the current share price and note it is presently less than the current cash backing per share… Should the share price remain around or near current levels and there is no material, non-public information, share buybacks will be undertaken.“

A small number of shares were repurchased before the blackout period, and chairman John McMahon has confirmed that buybacks will resume now that annual results have been released.

I’m not sure how successful the repurchases will be given the illiquidity of the stock, but it is clear this is the most effective way of using the large cash pile to maximize shareholder value.

Looking forward, I believe there is potential for large capital returns over the next couple of years. For now, management has chosen to maintain a sizable cash balance given the uncertainty surrounding the recent restructuring. However, as visibility improves, it seems likely that excess cash will be distributed as the business requires minimal reinvestment.

One additional catalyst for increased payouts is the expiration of a government grant. For the past three years, SDL received a New Zealand growth grand that required dividends to remain below 50% of net income. With this restriction set to end, the company will regain flexibility to return a much larger share of earnings and cash to shareholders.

Risks:

Small and illiquid.

Customer concentration: The top five customers contribute 55% of SDL’s revenue. Losing another major account would materially impact results.

Secular decline in print: The New Zealand mailhouse business is in long-term decline. Although the company has been successful in growing revenue through gaining market share as well as transitioning sales to its software product, it is clear this will not continue forever and growth is likely to slow in the future.

Competition: SDL competes against much larger global players. SDL seems to have carved out a niche utilizing its strong physical presence in New Zealand as well as strategic business partnerships to drive new business growth. If the company is unable to maintain these relationships it will adversely affect growth.

Restructuring impacts: Reduced sales and support teams could affect growth and customer satisfaction.

Why this mispricing exists:

Small and illiquid, with a NZ$10M market cap.

Misclassified as a declining print/advertising company rather than a capital-light, high ROIC software business.

No coverage or mentions anywhere online.

Difficult to buy this stock, especially for U.S. investors. I shared an outline of this idea to over 100 people, and the most common response was “I like it, but my broker won’t let me buy the stock”.

At the current valuation, this seems like a case of “heads I win, tails I don’t lose”: a large cash pile in excess of market cap covering the downside, and business recovery providing upside optionality.

Disc. Long shares of $SDL

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. Investing involves risk, including the potential loss of principal. The author may own, or plan to purchase, shares in the security discussed. The author is not a registered investment advisor and does not provide personalized investment advice. Always conduct your own research and consider your investment objectives and risk tolerance before making any investment decisions. The author and publisher shall not be liable for any actions taken based on the information provided in this article.

Great breakdown — the cash backing + buybacks definitely make SDL hard to ignore. What struck me is how the market still buckets it as ‘old print’ when the SaaS side is sticky, asset-light, and scaling internationally. The Pitney Bowes partnership looks like a real distribution lever, but the customer concentration risk is still glaring. Curious if you see this as a compounding software play that eventually earns a SaaS multiple, or if it’s more of a mean-reversion value setup with a capped upside?

Thanks for the article. The company is based a few km from where I live. While I don't know the company that well, I'm very familiar with most of the shareholders on the top shareholder list - it's a whose who of those in the sharebroking/investment community in NZ. The Chair is a smart guy - he was a top analyst when in sharebroking - and he's also a major shareholder. I'd be surprised if they can buy back much if any stock at all if they put a buyback program in place. Maybe they can make an acquisition as funds on deposit now earning less than 4% pa before tax isn't very efficient. It looks a 50/50 bet to me. I'm dubious on the ThreeWaters growth option, and the mortgage refinancing - well New Zealanders are all on short-dated housing loans, so yes there's a lot of that going on right now, as I think around 3/4 of NZ housing loans rollover in the next 12 months. For me, I think there are better small cap options in NZ - but if they can grow earnings again, it could easily pop as you say!