Microcap Trading at Cash Value, Inflecting Earnings, 15% Dividend Yield

Downside Protection with Asymmetric Upside

Today’s stock:

Microcap trading at net cash value

Consistent 15% dividend yield

Industry recovery and operational shift driving an earnings inflection

In my search through obscure OTC stocks, I’m drawn to names that are trading at a negative or near-negative enterprise values. These setups can be exceptional, as you’re essentially buying the operating business for free, with the market valuing only the cash on the balance sheet. If the company avoids existential risks and either returns capital or shows signs of growth, the upside can be explosive.

The stock I’m covering today is trading right around its cash value, while its core business is quietly inflecting earnings growth. Recovering earnings and capital returns with a 15% dividend yield creates a setup which offers the rare combination of downside protection and asymmetric upside.

If you like reading about undervalued stocks no one else is covering, Subscribe.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. Investing involves risk, including the potential loss of principal. The author may own, or plan to purchase, shares in the security discussed. The author is not a registered investment advisor and does not provide personalized investment advice. Always conduct your own research and consider your investment objectives and risk tolerance before making any investment decisions. The author and publisher shall not be liable for any actions taken based on the information provided in this article.

Overview:

Pharma-Bio Serv Inc. is a consulting firm specializing in regulatory compliance, validation, and technology services for pharmaceutical, biotech, and medical device companies.

Founded in 1993 in Dorado, Puerto Rico, the company has built a 30 year reputation as one of the leading pharmaceutical consulting firms globally. Its headquarters and primary operations remain in Puerto Rico, a key hub for pharmaceutical development and manufacturing.

In 2018, the company divested its unprofitable chemical testing lab to focus exclusively on its higher-margin consulting business.

Despite a tiny $11 million market cap, Pharma-Bio Serv serves some of the largest pharma and biotech companies in the world, including Zimmer Biomet, Baxter International, Thermo Fisher, and Johnson & Johnson.

Its workforce includes 75 employees and independent contractors that are experienced life science professionals and quality assurance directors.

Pharma-Bio Serv’s core business is regulatory compliance consulting for FDA and international agencies, ensuring that clients’ products and facilities meet strict regulatory standards. Other services include validation (testing and documenting equipment and systems), technology transfer (relocating manufacturing operations), and project management.

Its competitive advantage comes from a 30 year track record, deep entrenchment in the Puerto Rican pharmaceutical market, and a commitment to hiring high-caliber consultants that deliver superior outcomes for clients.

Revenues are somewhat cyclical, generally tracking the growth of the broader pharmaceutical industry. This is a quality business with a strong customer base and a history of consistent profitability.

Valuation:

In my view, this is a solid business trading at an exceptionally low valuation.

I believe the consulting business can generate normalized earnings of $2 million per year, consistent to what they earned after the lab divestment. While somewhat cyclical, its strong reputation in a durable industry demonstrates staying power. A conservative valuation for a small yet stable business such as this is around 5x earnings.

However, this overlooks the company’s substantial cash holdings.

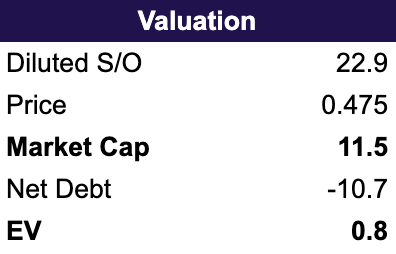

As of the last quarter, the company holds $10.7 million in cash post dividend against an $11 million market cap. This means the market is ascribing zero value to the operating business, which in normal market conditions can earn $2 million per year.

The valuation here is straightforward. I take into account full value of the cash holdings (for reasons I’ll outline below) and a 5x multiple on $2 million in earnings gives us a $21 million valuation, roughly double the current market cap.

Catalyst:

The Pharmaceutical and Biotech sectors have undergone a difficult period since 2021, when rich valuations, policy changes, and interest rate hikes triggered a significant bear market. From 2021 to 2022, the biotech industry experienced one of its steepest drawdowns on record, and major pharmaceutical and biotech indices remain well below their 2021 highs.

A combination of peak pessimism and data pointing towards growth this year suggests the industry is poised for a recovery.

Such a recovery would directly benefit Pharma-Bio Serv, as its business depends on industry spending for drug development and medical device manufacturing.

Signs of this inflection are beginning to show in the company’s financials. In Q1 of this year, Pharma-Bio Serv reported positive net income for the first time since September 2023, with management stating:

“we are poised for continued expansion as we drive growth by anticipating client needs”

In recent years, the company invested in technology upgrades and increased marketing spend, with these initiatives appearing to be paying off.

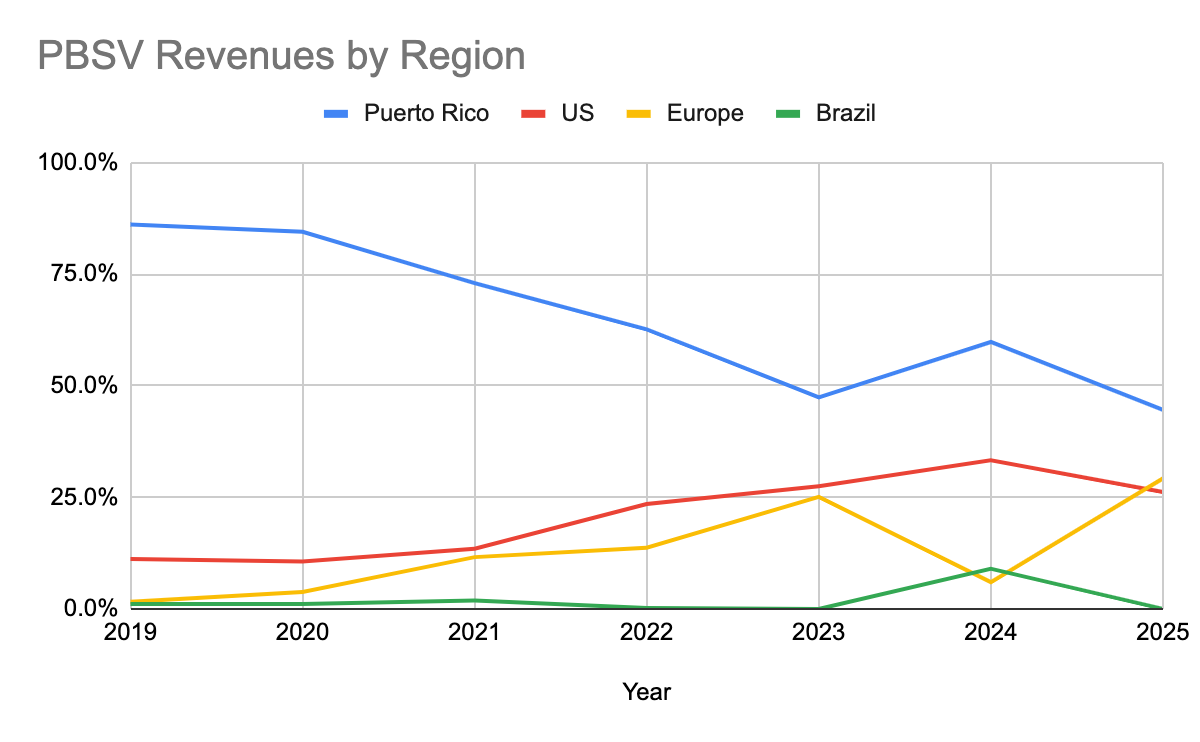

The company has also made operational changes to improve profitability. Notably, it has shifted its focus towards consulting projects in Europe, which management notes are higher margin. Here’s a breakdown of revenue by region since 2019.

European projects have grown from 0% of revenues in 2019 to over 25% today. This transition from lower-margin Puerto Rico projects to European consulting should gradually improve gross margins.

Additionally, since 2020 Pharma-Bio Serv has paid out a large annual dividend, distributing at least $1.7 million annually, with the most recent payout being last quarter. At today’s share price, this is a yield of 15%.

Beginning in 2023, the company also moved a significant portion of its cash into money market funds and Treasury bills yielding 4-5%. While I’d prefer this cash be returned to shareholders, it generates roughly $400,000 per year in additional income.

There’s been some critique of management for holding this large cash position for years, but five consecutive years of steady dividend demonstrate a consistent commitment to return capital to shareholders. This is also why I do not place a discount on the company’s cash balance in my valuation. Even without stock price appreciation, the dividend alone offers a 15% annual return.

Risks:

The CEO owns a negligible amount of stock, so he lacks financial alignment with shareholders. Company insiders in total own 12.6% of outstanding shares.

There’s a concern management could squander the cash on the balance sheet on poor investments, but this risk seems modest given the company’s track record.

The $250,000 investment in an AI company affiliated with a board member is not a good look, however I do not expect investments like this to continue and in this case it seems to benefit the company with a new system for business development and personnel recruitment.

The company held a Puerto Rico tax grant whose 15-year term ended in October 2024. This grant provided tax relief for business activities conducted within Puerto Rico. The company has applied for a renewal of this tax grant and expects it to be accepted (which is normally the case) but if this does not happen it could result in a higher tax rate.

A more significant risk is customer concentration. The company’s top three clients account for approximately 50% of revenue. This concentration exposes Pharma-Bio Serv to substantial downside if a major client leaves or renegotiates for lower fees. While the company enjoys strong, long-standing relationships with these clients, nothing prevents them from seeking cheaper alternatives or bringing compliance work in-house.

Industry consolidation is both a challenge and opportunity for the company. Larger pharmaceutical and biotech firms continue to acquire smaller companies, leading to a more concentrated customer base with greater bargaining power and potential R&D budget constraints. At the same time, this creates opportunity for Pharma-Bio Serv to secure consulting projects for post-merger integrations and outsourced compliance services.

The company also faces common microcap risks, such as illiquidity and limited analyst coverage.

With an average daily trading volume of around 3,500 shares over the past month, it’s possible to gradually build a position.

This is the type of company I look for. A large cash pile and 15% dividend yield capping your downside, and potential upside coming from an inflection in earnings or increased investor attention.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. Investing involves risk, including the potential loss of principal. The author may own, or plan to purchase, shares in the security discussed. The author is not a registered investment advisor and does not provide personalized investment advice. Always conduct your own research and consider your investment objectives and risk tolerance before making any investment decisions. The author and publisher shall not be liable for any actions taken based on the information provided in this article.

What about the revenue decline? They may be making more on their cash than on the business. I am always wary of a dividend yield that is unusually high. Be careful. I’ll pass. Hope I am wrong. Good luck.

Great find and thanks for sharing. $12M in retained earnings is good to see. 2025 could be the inflection year - worth a closer look.