Microcap Selling Loss-Making Subsidiary For More Than Enterprise Value

Divestiture Not Yet Reflected in Market Price

Summary:

Loss-making subsidiary sold for more than total enterprise value

Trading at 3x EBIT, Negative EV

Sale not yet reflected in reported financials

One of the main advantages of investing in microcaps is that there can be a meaningful lag before company announcements are fully reflected in market prices.

In these markets even meaningful corporate developments can be overlooked when a business operates at the smallest end of publicly traded companies.

Many of these companies operate with little investor attention, which can create situations where the market price lags underlying fundamentals.

Today’s stock announced a transaction which meaningfully improves the company’s financials, and yet the price hasn’t moved. The stock is invisible to screeners and has no mentions online.

Let’s get started…

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. Investing involves risk, including the potential loss of principal. The author may own, or plan to purchase, shares in the security discussed. The author is not a registered investment advisor and does not provide personalized investment advice. Always conduct your own research and consider your investment objectives and risk tolerance before making any investment decisions. The author and publisher shall not be liable for any actions taken based on the information provided in this article.

Overview

Escalon Medical Corp. (ESMC) is a niche manufacturer and distributor of ophthalmologic diagnostic and surgical equipment. Their products are used by eye doctors and surgeons to diagnose ocular conditions and perform medical procedures.

Escalon operates through three main product lines:

Sonomed

Sonomed is Escalon’s core business which manufactures ultrasound imaging devices used in ophthalmology. These systems allow physicians to see inside the eye for diagnostic purposes. Sonomed devices perform several key functions:

A-Scan: Measures distance inside the eye and is primarily used to calculate the correct lens for cataract surgery.

B-Scan: Produces 2D ultrasound images of the eye, used when vision is clouded due to blood or cataracts.

UBM (Ultrasound Biomicroscopy): High-resolution imaging of the front of the eye, used for complex conditions such as glaucoma and tumors.

Sonomed sales account for ~75% of the company’s total revenues and drives the majority of the company’s profitability. Revenue from this segment is lumpy due to long equipment replacement cycles and variability in capital spending by medical practices.

Trek

Trek is the company’s surgical consumables brand, selling intraocular gas products and sterile surgical packs which are used in eye surgery. The segment generates ~17% of total revenues and provides a more stable, recurring revenue stream compared to the company’s equipment business.

Axis

Escalon’s ophthalmic imaging software, which allows physicians to store diagnostic images, review scans, and integrate imaging data across devices and medical record systems.

Escalon has a long operating history, being founded in 1987 as a medical device distributor before transitioning into a niche ophthalmic equipment manufacturer following the acquisition of Sonomed. This transition was led by former CEO Richard DePiano Sr. who became CEO of the company in 1997.

Escalon remains effectively family controlled, with Richard DePiano Jr. succeeding his father as CEO in 2013 and holding 78% of voting shares.

The company is headquartered in Wayne, PA with manufacturing and distribution operations in New York and Wisconsin.

The ophthalmologic device market is a highly competitive industry dominated by significantly larger medical device manufacturers. Despite Escalon’s small scale, they have carved out a niche through decades-long relationships with independent eye surgeons and small hospitals.

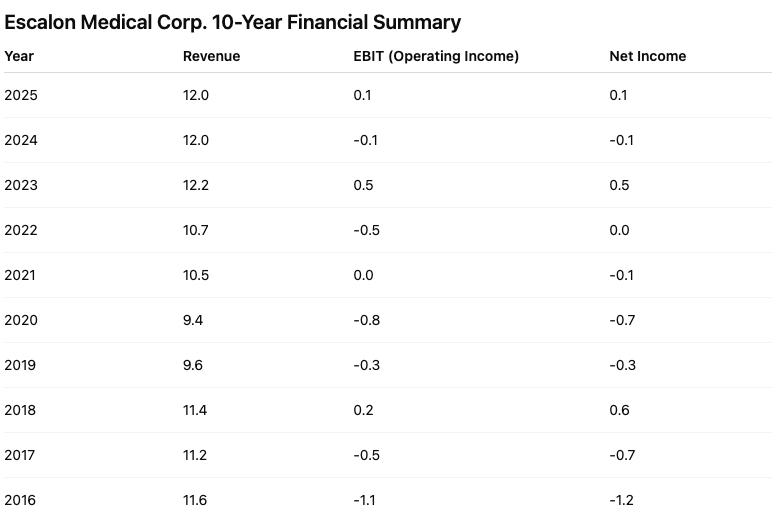

Escalon serves a market with steady, recurring demand as imaging devices need to be replaced and surgeries need to be performed. Over the past decade, revenue has remained stable, ranging between $10-12 million annually. Operating expenses have gradually decreased, allowing the company to operate near breakeven for the past eight years.

Catalyst

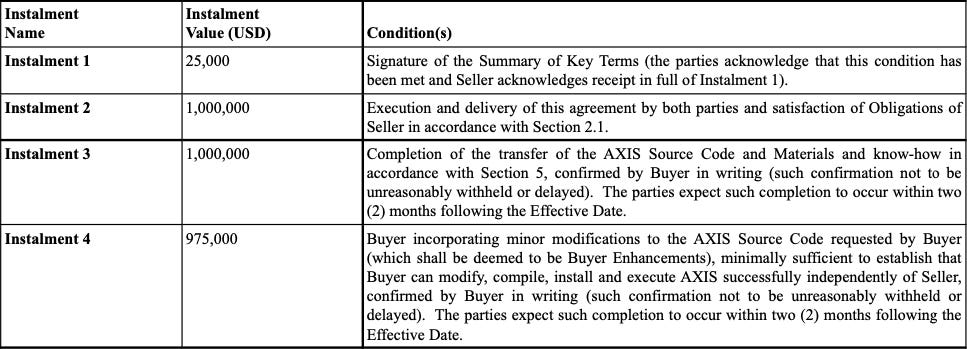

In August 2025, Escalon announced the sale of its Axis software to Optos Plc, a subsidiary of the Nikon Corporation, for a total price of $3 million.

The purchase price is contingent on three primary milestones, with the first milestone already completed. Escalon disclosed that it received the initial $1 million payment on January 23, 2026, leaving two remaining milestones outstanding.

I believe completion of the remaining milestones is highly likely, as they are primarily delivery-based and technical in nature, rather than dependent on financial performance.

Optos is a large strategic buyer that will benefit from this software and has already made the initial $1 million payment, and Escalon is in need of the cash so there is clear incentive on both sides for the deal to go through.

Both parties expect the remaining two milestones to be met within the next two months.

Impact on Operations

The divestiture of Axis will materially improve Escalon’s earnings profile.

For a company of Escalon’s size, supporting a standalone software platform created a structurally inefficient cost base. According to pro forma financials, the Axis segment generated $832K in revenue (7% of total revenue) in FY25, while producing an operating loss of ~$400K.

Although Axis contributed a small portion of total sales, it had a disproportional drag on profitability. By selling the segment, Escalon removes a meaningful source of operating losses while simplifying the business around its core ultrasound and surgical consumables operations.

Escalon has historically managed expenses well and has operated near breakeven since 2018. Earnings are somewhat variable due to equipment replacement cycles, but post-divestiture I estimate the company can generate $400K in normalized EBIT annually.

Valuation

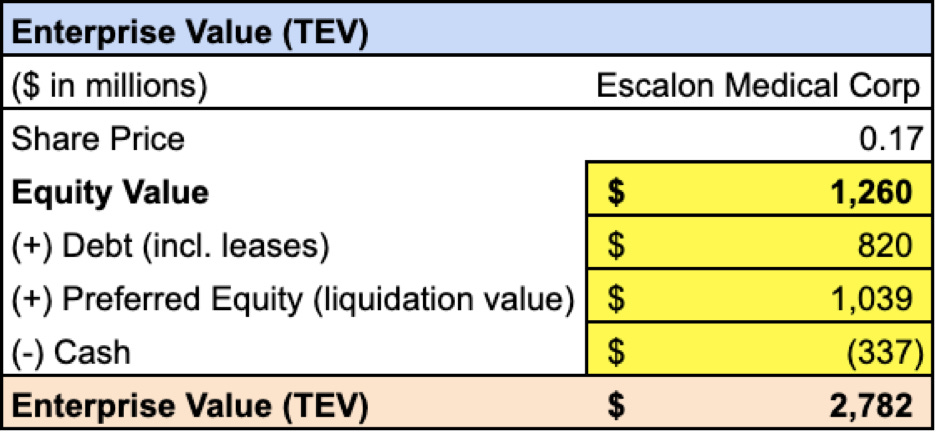

Escalon trades at an extremely depressed valuation relative to both its operating business and projected post-transaction balance sheet.

Importantly, the most recent reported financial statements do not reflect the initial $1 million payment received from the Axis transaction.

Assuming Escalon receives the full $3 million purchase price, the company would trade at a negative enterprise value and ~3x EBIT.

The company has $29.5M in NOLs that can be used to offset taxes from the Axis sale as well as future operating income.

I believe 5x EBIT is a reasonable valuation for the operating business. Applying this multiple and adding projected net cash results in an implied stock price of $0.61 per share, which represents over 250% upside from todays price.

Why this mispricing exists

Escalon is a $1.2M market cap company which means there is an extremely limited investor pool with no activity from institutional investors.

In addition, there is a temporary disconnect between the company’s reported financial statements and its actual economic condition. While Escalon disclosed receiving the initial $1 million Axis payment, this cash has not yet appeared on the company’s balance sheet due to reporting timing.

A potential catalyst may be the publication of updated financial statements reflecting the improved balance sheet, which will likely be released this month.

Risks

Final installments of Axis sale are not paid

My assumptions about future profitability are wrong

CEO owns 78% of voting shares, limiting minority shareholder influence

Poor capital allocation

Small and illiquid stock

As previously mentioned I think it is unlikely the deal falls apart, as both sides are incentivized to complete it.

The other main risk here is operational execution. Even after selling Axis, Escalon remains a small company in a competitive industry with unpredictable revenue. It is possible the company struggles to generate sustainable profitability despite removing a loss-making segment.

Another important thing to note is that Escalon is essentially a family controlled business, with DePiano Jr. succeeding his father as CEO after decades of leadership. Historically management have operated the company conservatively and avoided taking large risks.

There have been shareholder concerns in the past around the company’s debt exchange agreement in 2018 which led to significant dilution, as well as compensation agreements related to DePiano Sr.’s retirement package. While these issues are worth noting, management’s behavior in recent years has been much more shareholder friendly and operationally disciplined.

In cases such as this, it is likely preserving the family legacy matters more than attempts at aggressive expansion. I believe Escalon’s management will use the Axis proceeds to pay off remaining debt and preserve capital for operational stability rather than pursue risky acquisitions or expansion efforts.

I also believe the Axis divestiture increases the likelihood of a full sale of Escalon in the near future. Escalon does not possess the capital to continue to advance their products in line with competitors, and the sale of the software division considerably simplifies the remaining business.

In the event of a sale Escalon could fetch substantial upside, with the company currently trading at .1x revenue. This is a valuation that appears disconnected from transactions of medical device companies. Even a takeout at a heavily discounted revenue multiple could result in a sale price several times higher than the company’s current market cap.

Conclusion

This is a situation where a meaningful improvement in Escalon’s financial position has not yet been reflected in its stock price. As the transaction is completed and incorporated into reported financials, I expect the gap between market price and intrinsic value to close.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. Investing involves risk, including the potential loss of principal. The author may own, or plan to purchase, shares in the security discussed. The author is not a registered investment advisor and does not provide personalized investment advice. Always conduct your own research and consider your investment objectives and risk tolerance before making any investment decisions. The author and publisher shall not be liable for any actions taken based on the information provided in this article.

Could you explain how you got 400k normalized yearly EBIT and your valuation multiple as well. Do u think it would be better to do a dcf to cross check the multiple