Fast-Growing Software Company, 9x FCF, Buying Back Shares

Growing fast, highly profitable, and returning cash to shareholders

Summary:

Profitable, fast growing software company

9x FCF

Buying back stock

Strategic sale likely

Sometimes the market is driven more by fear than fundamentals.

Panic selling can push even high-quality businesses far below their intrinsic value, not because the company is weak, but because sentiment and short-term pressures dominate.

These moments often create the best buying opportunities. When selling is driven by panic, patient investors can step in and buy high-quality companies at unusually attractive prices.

Today’s stock has been caught in the recent software sell-off, where broad fear has depressed valuations across the sector.

Its fundamentals remain solid: profitable, growing, and capital-light, with a sticky business model that generates recurring revenue.

For long-term investors, the market’s panic presents a rare chance to buy a high-quality software business at an attractive entry point.

Lets dig in…

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. Investing involves risk, including the potential loss of principal. The author may own, or plan to purchase, shares in the security discussed. The author is not a registered investment advisor and does not provide personalized investment advice. Always conduct your own research and consider your investment objectives and risk tolerance before making any investment decisions. The author and publisher shall not be liable for any actions taken based on the information provided in this article.

Note: All figures in $CAD

Overview:

NamSys Inc. (CTZ.V) provides software that helps businesses manage and track physical cash.

The company operates across three main revenue lines:

Currency Controller (38% of revenue)

NamSys’ core cash-processing software, used by banks and cash-processing centers. This platform handles the counting, sorting, and reconciliation of physical cash balances. This software is critical for the highly regulated industry it serves.

Cirreon Retail (40% of revenue)

Cash-management software for retailers that connects to smart safes and cash registers. It automates cash balancing and reporting, providing real-time visibility into cash levels. This saves staff time by eliminating manual cash counts and reduces errors.

Cirreon CIT (22% of revenue)

Logistics software for armored car and cash-in-transit providers. It tracks pickups and deliveries, optimizes routes, and provides live reporting to the cloud. This replaces paper logs and makes cash transportation more secure and efficient.

Cirreon CIT is NamSys’ fastest-growing product, with revenue growing 52% in FY24. This growth is driven by banks facing pressure to streamline operations and cut costs, leading them to outsource cash processing and transportation to third-party providers that rely on NamSys’ software.

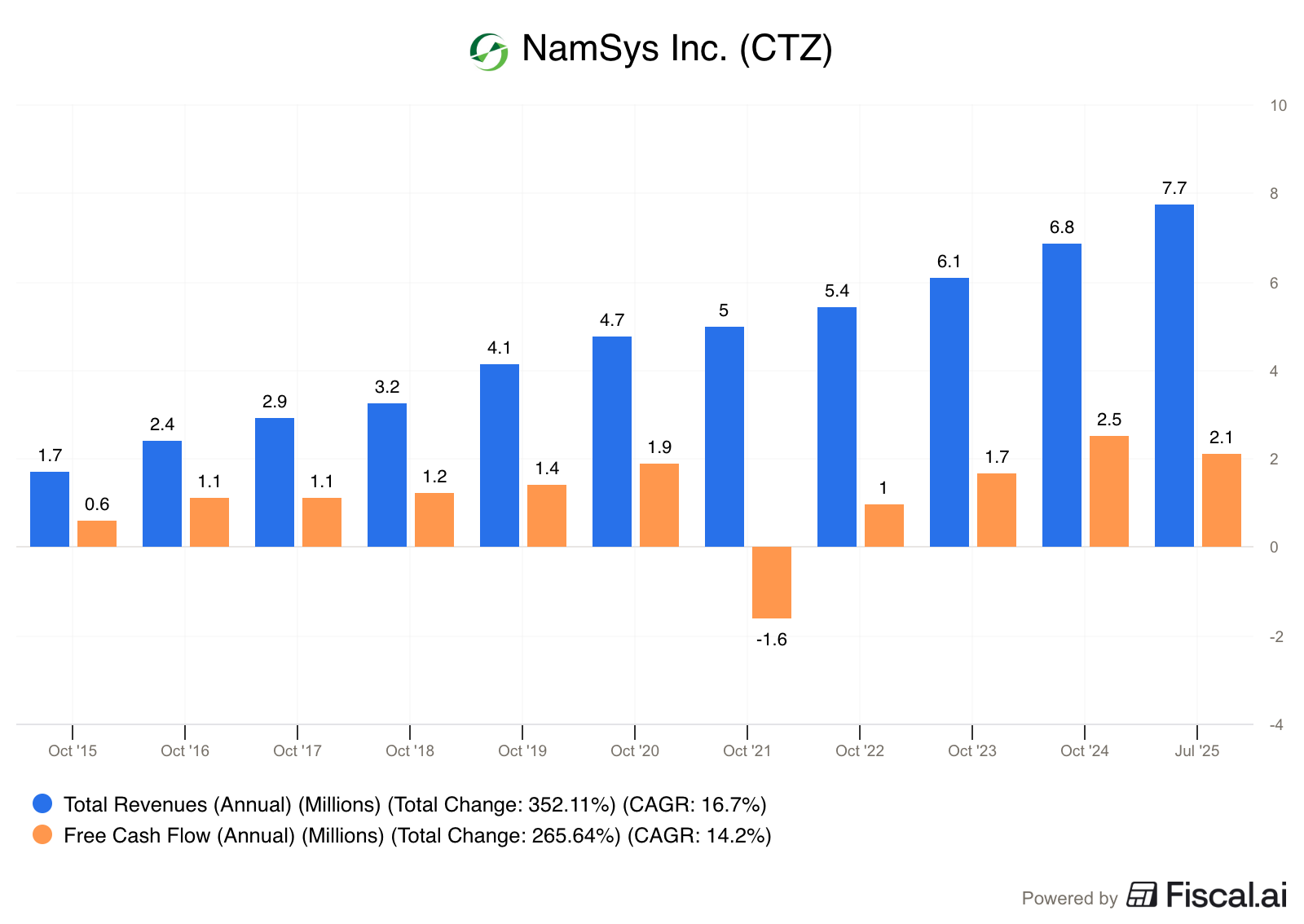

Despite cash management being thought of as a dying industry, NamSys has grown both revenue and free cash flow at double digit rates over the past decade.

The business is capital-light and efficiently run with only 18 employees, resulting in high returns on capital and 31% net margins.

Growth Drivers

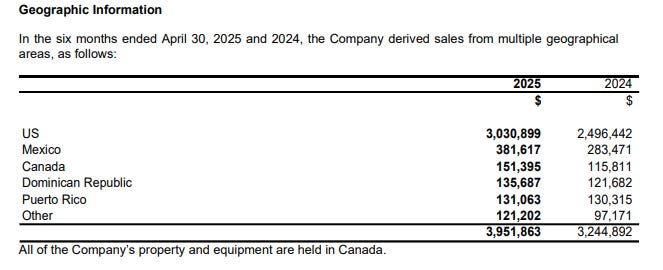

Despite being a Canadian company, NamSys operates primarily in the United States, with 96% of revenue collected in U.S. dollars.

Revenue growth has been driven by:

Expanding its U.S. customer base

Selling add-ons to existing customers

International expansion, particularly into Mexico, which now represents roughly 10% of total revenue

Management recently noted the addition of a new hire dedicated exclusively to growing the business outside the United States, with early progress already underway. This increases the likelihood that international revenue continues to grow as a meaningful portion of the business.

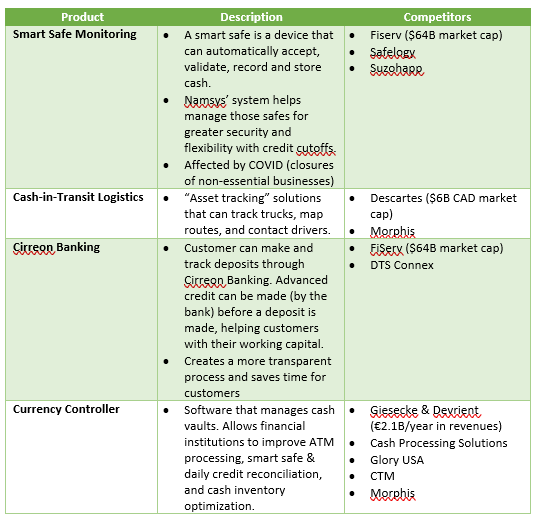

Competition:

Despite a market cap of only $29M, NamSys competes against much larger companies across each of its product lines. Here is a chart from a 2021 VIC writeup which shows the competitive landscape:

NamSys is able to compete effectively by focusing on smaller, independent operators and offering greater flexibility than larger enterprise vendors. Customer retention is exceptionally strong, with virtually no churn across its software offerings.

While larger competitors could theoretically develop competing products, NamSys’ entire market capitalization is a fraction of their annual revenues, making the opportunity unattractive. Given the cost and complexity of developing comparable software, acquiring NamSys would be far more likely than trying to outcompete them.

Capital Allocation

As a result of years of profitable growth, NamSys has accumulated a substantial net cash position equal to roughly one-third of its current market cap.

Management has generally been good stewards of capital. Since 2014, the company has eliminated all debt, redeemed its preferred shares, and bought out a long-term employee bonus plan in 2021.

This bonus plan was poorly structured and scaled as the company grew, so eliminating it was a shareholder-friendly decision.

I believe a key inflection point came in 2022 when Gabriel Bouchard-Phillips joined the board. As a partner at a small-cap focused investment firm, his involvement likely helped push management toward more shareholder-friendly capital returns.

Since then, the company has paid a large special dividend in 2024 and approved a share repurchase program for up to 5% of outstanding shares in 2025.

Management has consistently stated that their primary objective is to make a strategic acquisition that enhances growth and increases NamSys’ attractiveness to potential acquirers. At the most recent shareholder meeting, management said:

“Our goal is still an acquisition. We have had meaningful discussions over the past 12 months, but unfortunately have not made anything really work. The standards that we have are quite high…And we think that [a strategic acquisition] will generate ultimately more value for shareholders in the event of an acquisition by a third party of NamSys”

This strategy makes sense, as strategic buyers are likely to value growing revenue streams more highly than excess cash.

Management’s patience in looking for a suitable acquisition target suggests they are unlikely to pursue a value-destructive acquisition simply to grow in size.

The recent dividends and buybacks also make it seem likely that if a suitable acquisition does not materialize, excess cash will continue to be returned to shareholders.

Valuation:

Price: $1.07

Market Cap: $28.7M

Enterprise Value: $19M

LTM FCF: $2.11M

EV/FCF: 9x

A single-digit free cash flow multiple is too low for a business of this quality and growth profile.

The current discount is likely driven by a combination of limited liquidity (30% free float) and the broader sell-off in public software companies.

Despite being far higher quality than many software peers, NamSys has been caught in this indiscriminate selling, losing approximately 33% of its value over the past five months.

Historically, the company trades around 15x FCF. This gives investors a meaningful margin of safety at the current valuation. Assuming free cash flow continues to grow at 10–15% annually, this implies a double-digit IRR even without multiple expansion.

I believe the most likely endgame is an acquisition. In that scenario, upside could be significantly higher, particularly if NamSys completes a complementary acquisition that accelerates revenue growth.

Risks

Terminal value: The most commonly cited risk with NamSys is that physical cash handling is a structurally declining industry. I believe this risk is overstated. Cash remains useful in many contexts, and cash usage in the United States has remained stable at approximately 16% of transactions since 2020. Additionally, NamSys is expanding into markets such as Mexico, where roughly 60% of transactions are conducted in cash.

Customer Concentration: NamSys’ largest customer is Brinks. Revenue from Brinks has declined from 40% of total revenue in 2020 to approximately 20% in 2024. Continued growth in the U.S. and international markets should offset any further declines from Brinks over time.

Foreign exchange: Namsys collects 96% of revenues in U.S. dollars yet reports financials in Canadian dollars, which creates the risk of currency fluctuations. This is the main driver for the decline in FCF over the past 12 months.

Forced Sellers: Executive Chairman Barry Sparks passed away in January 2025. His estate holds 8 million shares, roughly one-third of the company, and has been gradually selling its position. Continued selling may keep the stock price artificially depressed due to limited liquidity. However, this has no impact on underlying business fundamentals and may provide attractive entry points.

Small and Illiquid: Common microcap risks apply.

Conclusion

At $1.07 per share, NamSys offers the opportunity to own a fast-growing, highly profitable software business at an attractive valuation.

I believe the setup offers a strong probability of double-digit IRRs. Even if my assumptions about future growth or valuation prove wrong, the risk of a permanent loss of capital appears limited at today’s price.

Disc. Long shares of NamSys

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. Investing involves risk, including the potential loss of principal. The author may own, or plan to purchase, shares in the security discussed. The author is not a registered investment advisor and does not provide personalized investment advice. Always conduct your own research and consider your investment objectives and risk tolerance before making any investment decisions. The author and publisher shall not be liable for any actions taken based on the information provided in this article.

How do you see Management executing here? I mean they‘ve been searching for an acquisition for quite some time. They could sit on the cash for another 3-4 years.

With the software sector being down, there could be a possibility that we don’t see a multiple expansion to the old figures we’re used to see.

That's a very interesting analysis on NamSys that was not on my radar at all. When you see these small cap businesses forming fundamental strength it can be one of the best investments to make. Curious to see if the financials continue to reveal a pattern that underlines this strength.